US Aerostructures Market Report: Size, Share & Competitive Landscape 2026–2035

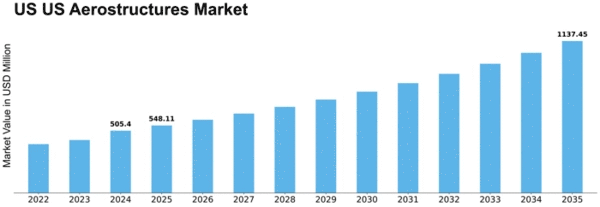

As per analysis, the US Aerostructures Market is projected to grow from USD 505.4 Million in 2024 to USD 1137.45 Million by 2035, exhibiting a compound annual growth rate (CAGR) of 7.65% during the forecast period (2025 – 2035).

Introduction

The aerospace industry represents one of the most strategically important and technologically advanced sectors of the U.S. economy. A critical component of this sector is the aerostructures segment, which includes the design, development, and manufacturing of aircraft structural components such as fuselages, wings, empennages, control surfaces, and other load-bearing elements. With rising global air travel demand, defense modernization efforts, and increasing complexity of aircraft platforms, the US Aerostructures market is poised for strong growth over the next decade.

In the United States, aerostructures are produced by a mix of OEMs, tier-1 suppliers, and specialist fabrication firms leveraging cutting-edge materials like composites and advanced alloys. U.S. manufacturers are focusing on weight reduction, production efficiency, and manufacturing automation—key drivers that help make American aerospace products competitive on the global stage.

Market Growth and Trends

Several macroeconomic and industry-specific trends are shaping the growth of the US aerostructures market:

- Growing Commercial Aviation Demand

The global appetite for air travel is steadily climbing as passengers return to pre-pandemic travel levels and airlines expand fleets. U.S. carriers are investing in new aircraft, stimulating demand for advanced aerostructures. - Defense Modernization and Procurement

U.S. defense initiatives including next-generation fighters, transport aircraft, and unmanned systems continue to require sophisticated aerostructures. Defense spending, while cyclical, provides a stable long-term backbone for the market. - Advanced Materials and Composites

Lightweight materials, especially carbon-fiber reinforced polymers and new metal alloys, are increasingly used to improve fuel efficiency, strength, and durability. The U.S. aerostructures sector is at the forefront of these innovations. - Additive Manufacturing and Automation

Manufacturers are adopting robotics and 3D printing to reduce waste, improve precision, and shorten lead times. This trend enhances competitiveness and creates new pathways for custom and highly engineered parts.

Key Players

The US aerostructures landscape features a blend of large aerospace OEMs, major Tier-1 suppliers, and specialized fabricators. Key participants typically include:

- Leading OEMs who integrate aerostructures into complete platforms and influence supply chain direction

- Tier-1 Suppliers engaged in high-volume production of wing assemblies, fuselage sections, and other critical components

- Specialty Material Firms delivering cutting-edge composite materials, coatings, and structural technologies

These players compete and collaborate through joint ventures, long-term contracts, and strategic alliances to meet airline and defense requirements while maintaining compliance with rigorous safety and regulatory standards.

Future Scope

The outlook for the US Aerostructures Market remains robust across multiple dimensions:

- Continued defense spending is expected to sustain demand for complex aerostructures in next-generation military platforms.

- Commercial aviation growth will fuel long-term production needs, particularly in efficient narrow-body and wide-body aircraft.

- Investment in sustainable aviation, including hybrid-electric and hydrogen propulsion systems, will drive innovation in structural design and materials engineering.

- Supply chain digitalization and resilient logistics systems will reduce risk and enhance responsiveness to market fluctuations.