Global Automotive Wheel Speed Sensor Market Analysis, Industry Trends and Forecast Report

Global Automotive Wheel Speed Sensor Market Set for Robust Growth, Driven by Mandatory Safety Regulated Architectures and Advanced Driver Assistance Systems (ADAS) Integration

New Comprehensive Strategic Analysis by Maximize Market Research Projects Significant Market Expansion Across Passenger and Commercial Vehicle Segments as Next-Generation Active Hall-Effect and Magneto-Resistive Sensors Take Center Stage globally.

The global automotive sector is undergoing a profound structural transformation, pivoting from mechanical configurations to smart, sensor-driven electronics. At the core of this safety and intelligence evolution is the critical component that bridges tire traction with computer logic: "Global Automotive Wheel Speed Sensor Market: Industry Analysis, Market Size, Share, Trends, and Forecast."

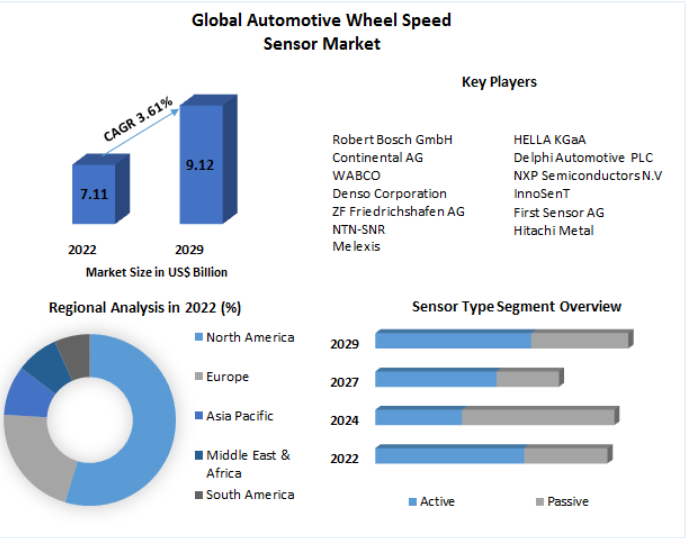

The study reveals that the global automotive wheel speed sensor market is positioned to ride an unprecedented wave of technological integration. Valued securely within the multi-billion-dollar tier, the industry is accelerating toward a highly lucrative forecast horizon. This growth is underpinned by an aggressive compound annual growth rate (CAGR) that signals immense potential for component manufacturers, Tier-1 suppliers, semiconductor companies, and automotive original equipment manufacturers (OEMs).

As automated breaking infrastructure, vehicle electrification, and software-defined chassis become baseline expectations for global car buyers, the demand for highly precise, ultra-reliable wheel speed tracking solutions has shifted from premium feature tiers to mandatory production architectures.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/29062/

The Strategic Trajectory: Market Size, Valuation, and Growth Velocity

To appreciate the sheer scale of the automotive wheel speed sensor market, one must examine the macroeconomic factors and volume dynamics currently shaping vehicle manufacturing lines. According to the strategic analysts at Maximize Market Research, the market's current multibillion-dollar footprint is not merely a reflection of steady vehicle assembly volumes, but rather an indicator of the rising "sensor density" per individual vehicle chassis.

Historically, a standard automobile might have utilized simplified, passive sensing systems restricted exclusively to the primary braking axle. In contrast, modern vehicle architectures demand dedicated, high-fidelity active sensors at all four wheels, often tied directly to independent electronic control units (ECUs). This tripling or quadrupling of electronic component value per vehicle is a core structural driver.

The report's quantitative multi-variable predictive modeling demonstrates a stable, upward trajectory. This path is fueled by the robust economic revival of automotive manufacturing hubs post-supply-chain stabilization, paired with burgeoning middle-class vehicle adoption rates across developing economic regions. Over the extended forecast window, this compounding demand curve is projected to unlock billions of dollars in incremental revenue opportunities, providing clear financial justification for intense corporate R&D asset allocations.

Catalysts of Growth: Unpacking the ADAS and Safety Imperative

The primary operational force propelling the automotive wheel speed sensor market is the sweeping integration of Advanced Driver Assistance Systems (ADAS). Modern driver safety features are no longer isolated sub-systems; they operate as interconnected networks that require absolute spatial awareness and real-time situational tracking.

Wheel speed sensors act as the primary biological nerve endings for these systems. They generate continuous, high-frequency data matrices detailing exactly how fast each wheel rotates relative to the others and the vehicle body.

-

Anti-lock Braking Systems (ABS): The fundamental foundation of modern vehicle safety relies heavily on wheel speed sensors to detect immediate wheel lock-up during emergency stopping sequences, automatically pulsing brake fluid pressure to preserve steering capabilities.

-

Electronic Stability Control (ESC) and Traction Control Systems (TCS): These systems analyze high-resolution data streams to identify microscopic wheel slips, instantly adjusting individual wheel torque and braking forces to counteract dangerous oversteer or understeer events.

-

Adaptive Cruise Control and Intelligent Parking Infrastructure: Modern driving automation features require micro-accurate, low-velocity data to execute smooth stop-and-go maneuvers in dense urban environments without driver intervention.

As international consumer awareness regarding road safety spikes, the presence of these intelligent stabilization ecosystems has become a decisive factor in vehicle purchasing behavior. Consequently, automakers are actively racing to standard-equip even their entry-level, budget-conscious vehicle variants with advanced sensor suites, expanding the total addressable market (TAM) for component manufacturers.

Decoupling Sensor Technologies: The Dominance of Active Sensing Systems

From a deeply technical engineering standpoint, the global automotive wheel speed sensor market is characterized by an irreversible technological migration away from passive sensor architectures toward high-performance active sensor variants. Understanding this technological bifurcation is absolutely essential for investment decision-makers and components buyers.

Passive Wheel Speed Sensors

Passive sensors, often operating on variable reluctance principles, utilize an internal permanent magnet wrapped carefully in copper wiring. As a slotted metallic tone wheel rotates past the sensor face, it alters the surrounding magnetic field, inducing an alternating current (AC) voltage signal. While inherently cost-effective, highly durable, and requiring no external power supply, passive sensors suffer from a major operational limitation: their signal strength is directly proportional to wheel speed. At ultra-low speeds or total stops, the signal degrades entirely, leaving the vehicle's onboard computers functionally blind during critical low-velocity maneuvers.

Active Wheel Speed Sensors

Active sensors utilize advanced semiconductor elements—primarily based on the Hall Effect or Magneto-Resistive (AMR/GMR) principles. These units require an external power source but provide an invaluable operational advantage: they deliver a clean, digital square-wave signal that remains perfectly stable down to zero miles per hour. Furthermore, next-generation active sensors do not merely track rotational velocity; they can detect the precise direction of wheel rotation (forward versus reverse) and even measure air-gap distances between the sensor head and the encoder ring.

The report by Maximize Market Research confirms that the active sensor segment holds an overwhelming majority of the global market share and will continue to expand its dominance. The demand for autonomous valet parking, hill-start assist, and sophisticated regenerative braking systems in new electric vehicles renders legacy passive tech obsolete for future-facing vehicle programs.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/29062/

Segmentation Blueprint: Passenger Cars vs. Commercial Fleets

The global automotive wheel speed sensor market exhibits distinct consumption patterns when segmented by vehicle type, with each vertical presenting unique volume profiles and technical specifications.

The Passenger Vehicle Segment

Passenger vehicles comprise the largest single volume share within the global market. The sheer sheer volume of global passenger car assemblies—encompassing sedans, hatchbacks, crossovers, and sport utility vehicles (SUVs)—ensures a massive, continuous demand base. In this space, sensor design priorities focus intensely on extreme miniaturization, lightweight structural materials to support vehicle range optimization, and cost-effective high-volume manufacturability. The rapid electrification of passenger fleets globally further accelerates this trend, as electric drivetrains require instantaneous wheel-speed inputs to manage electric motor torque response times, which are vastly faster than internal combustion engines.

The Commercial Vehicle Segment

Though lower in absolute unit volume compared to passenger cars, the commercial vehicle segment—comprising light commercial vehicles (LCVs), heavy-duty freight trucks, logistics fleets, and public transit buses—represents a highly lucrative, premium-value sector. Commercial vehicle wheel speed sensors operate under immensely harsh environmental conditions, enduring high vibrational stress, extended thermal cycles from heavy payloads, and relentless exposure to road debris and corrosive chemical agents. Consequently, sensors in this segment carry a significantly higher average selling price (ASP), as they must feature advanced heavy-duty housings, specialized moisture sealing, and robust electrical shielding to prevent fleet downtime.

Regional Strongholds: Mapping Global Demand Hotspots

A geographic deep-dive into the global automotive wheel speed sensor market highlights a highly dynamic landscape, where different regions present varied regulatory frameworks, production capacities, and technological adoption speeds.

The Asia-Pacific region stands as an absolute powerhouse within the global market, commanding the largest regional market share. This dominance is anchored firmly by China, which continues its reign as the world’s largest automotive market by both vehicle production and domestic sales. Additionally, India’s flourishing automotive manufacturing ecosystem, combined with Japan and South Korea's long-standing legacies in high-tech automotive electronics, makes Asia-Pacific an incredibly vital region.

The region’s growth is driven by the rapid expansion of domestic manufacturing capacities, government-backed incentives for clean-energy vehicles, and a massive, growing middle-class population hungry for technologically advanced personal mobility options.

Europe: The Technological Vanguard

Europe remains a vital cornerstone of the automotive wheel speed sensor market, characterized by an uncompromising commitment to premium vehicle engineering and pioneering safety technologies. The region is home to some of the world’s most prestigious luxury automakers and influential Tier-1 automotive suppliers.

The European market is heavily driven by stringent regulatory frameworks and exceptionally high vehicle evaluation standards, such as the Euro NCAP safety rating protocols. These strict testing benchmarks make it virtually impossible for an OEM to achieve a coveted five-star safety rating without incorporating comprehensive, next-generation active safety sensor systems as standard equipment across all model ranges.

North America: The High-Value Fleet and Innovation Hub

The North American market, led predominantly by the United States, is experiencing rapid growth, particularly in the adoption of premium active sensor technologies. The market dynamics here are uniquely defined by an overwhelming consumer preference for large passenger trucks, high-capacity SUVs, and extensive commercial shipping fleets.

Furthermore, North America serves as a primary global incubation hub for autonomous driving technology testing and validation. The rapid scaling of Level 2+ and Level 3 autonomous driving features in consumer vehicles, alongside the development of driverless commercial freight networks, ensures a high-value, tech-dense market for advanced wheel speed monitoring systems.

Regulatory Frameworks: The Invisible Hand Driving Market Mandates

Market forces alone are not the sole determinants of the wheel speed sensor industry’s rapid expansion; legislative mandates enacted by international governing bodies play an equally massive role. Governments worldwide are actively weaponizing regulatory compliance to drastically reduce road traffic fatalities and urban accidents.

For instance, foundational mandates requiring anti-lock braking systems (ABS) on all new passenger vehicles have been standard practice across major developed nations for years. However, contemporary legislative focus has shifted toward more advanced active prevention systems. Regulatory agencies in regions like the European Union, the United States, Japan, and South Korea have introduced sweeping rules making Electronic Stability Control (ESC) and Autonomous Emergency Braking (AEB) mandatory for all new vehicle approvals.

Because these critical safety networks are completely dependent on the unflinching, uninterrupted delivery of real-time data from the wheels, these legislative actions create an absolute, legal baseline of demand that insulates the wheel speed sensor market from broader economic volatility. Even during periods of fluctuating vehicle sales, the per-vehicle sensor count remains legally locked at maximum capacity.

Competitive Matrix: Innovation and Strategic Consolidation

The global automotive wheel speed sensor market features a highly competitive landscape dominated by prominent, globally established Tier-1 automotive component manufacturing corporations and specialized semiconductor innovators. Key industry leaders profiled within contemporary market discussions include:

-

Robert Bosch GmbH

-

Continental AG

-

DENSO Corporation

-

ZF Friedrichshafen AG

-

Sensata Technologies, Inc.

-

NXP Semiconductors N.V.

-

Infineon Technologies AG

-

TE Connectivity

-

BorgWarner Inc.

-

Hitachi Astemo, Ltd.

To maintain market dominance and safeguard their hard-won market shares against agile, low-cost regional competitors, these industry titans are executing aggressive multi-pronged strategic initiatives. Companies are pouring immense capital reserves into research and development to create sensors that exhibit unprecedented levels of environmental resilience, self-diagnostic capabilities, and cross-system integration.

Furthermore, strategic mergers, acquisitions, and long-term joint-venture partnerships between Tier-1 mechanical hardware manufacturers and specialized microelectronics developers are accelerating, ensuring a highly integrated supply chain capable of delivering turnkey intelligent chassis systems to automotive OEMs.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/global-automotive-wheel-speed-sensor-market/29062/

Strategic Recommendations for Executives and Corporate Decision-Makers

For corporate executives, procurement specialists, and institutional investors navigating the complexities of the automotive electronics landscape, the insights delivered within Maximize Market Research’s comprehensive study provide an invaluable roadmap for long-term strategic decision-making.

1. Accelerate the Sunset of Passive Portfolios

Component manufacturers must decisively pivot away from legacy passive sensor production lines. Capital allocations should be aggressively funneled into expanding the manufacturing capacities of advanced active Hall Effect and magneto-resistive sensor configurations to perfectly align with future OEM vehicle design requirements.

2. Deepen Semiconductor Supply Chain Partnerships

Given that modern active wheel speed sensors rely heavily on integrated circuits (ICs) and specialized semiconductor elements, Tier-1 automotive suppliers must cultivate robust, resilient, and multi-sourced long-term supply agreements with semiconductor foundries. This proactive positioning is vital to shield production schedules from potential global chip allocation disruptions.

3. Engineer for Electric Vehicle Architectures

R&D engineering teams should deliberately optimize sensor designs to cater to the specific mechanical requirements of electric drivetrains. This involves engineering sensors with higher signal resolution to effectively support ultra-fast regenerative braking calibration and designing specialized electromagnetic interference (EMI) shielding to protect sensor signals from the heavy electrical fields generated by massive EV battery packs and high-voltage power inverters.

Future Horizons: Electrification, Smart Tires, and Beyond

As the automotive sector speeds toward an increasingly autonomous, electric, and hyper-connected future, the humble wheel speed sensor is poised for a dramatic evolutionary upgrade. The industry is currently witnessing early-stage exploratory research into the realm of "smart tires" and completely integrated wheel hub assemblies.

Future product life cycles will likely see wheel speed sensors seamlessly combined with Tire Pressure Monitoring Systems (TPMS) and sophisticated tri-axial accelerometers into a single, cohesive, wireless intelligent hub unit. This next-generation integration will allow the vehicle to not only track speed and direction but also continuously calculate real-time tire wear, dynamically analyze changing road surface friction characteristics, and instantly communicate road condition anomalies directly to cloud-based municipal traffic networks.

By transforming from a simple rotational counter into a highly sophisticated predictive data asset, the wheel speed sensor will solidify its position as an completely indispensable pillar of tomorrow's global intelligent transportation infrastructure.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656