5G Infrastructure Market: Telecom Modernization Boosts Infrastructure Investments

Global 5G Infrastructure Market to Explode at a Staggering 49.8% CAGR, Reaching USD 149.85 Billion by 2030 as Telecommunications Shift to Cloud-Native Standalone Networks

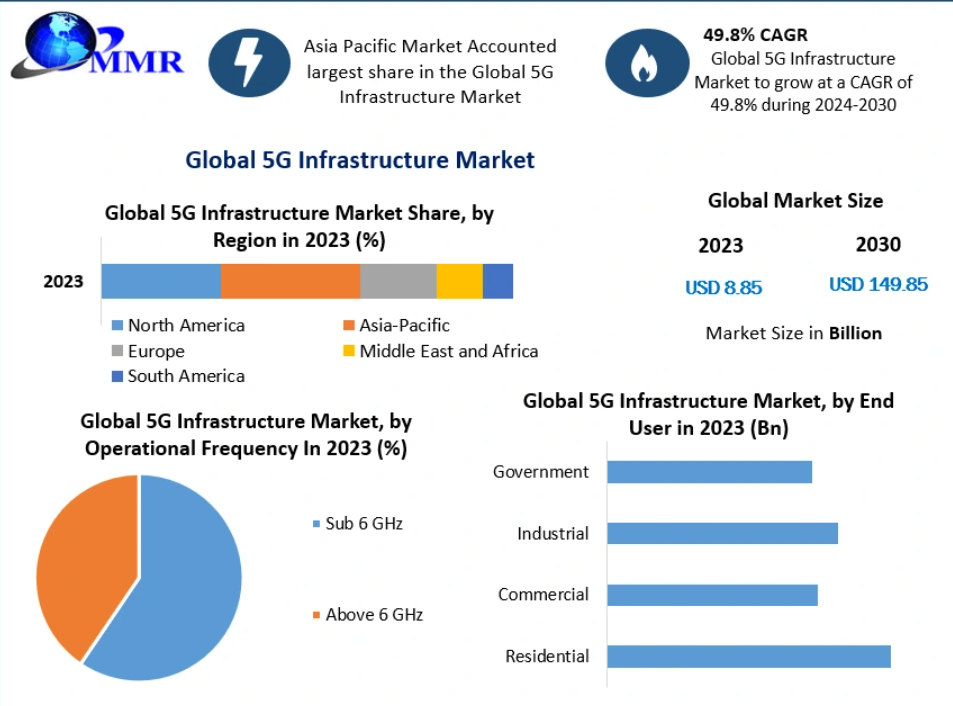

The global telecommunications sector is experiencing a monumental transformation as legacy physical networks give way to software-defined, hyper-scalable infrastructure. Driven by an urgent corporate need for ultra-low latency, skyrocketing data consumption, and rapid industrial digitization, the Global 5G Infrastructure Market is expanding at an extraordinary pace. According to the latest comprehensive market intelligence report released by Maximize Market Research, the industry was valued at USD 8.85 Billion in 2023. Moving forward, the market is projected to grow at an incredible compound annual growth rate (CAGR) of 49.8%, climbing to an estimated global valuation of USD 149.85 Billion by 2030.

This comprehensive multi-page industry study maps out how the deployment of advanced small and macro cells, software-defined networking (SDN), and network function virtualization (NFV) is rewriting standard economic models. It details how communication service providers (CSPs) and enterprise leaders can navigate this high-growth ecosystem to make informed capital allocations and data-driven strategic decisions.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/15292/

Executive Summary: The Backbone of the $1.3 Trillion Digital Economy

The roll-out of 5G infrastructure is no longer just a telecommunications upgrade—it serves as the baseline fabric for the next generation of global industry. While 4G networks successfully brought high-speed internet to smartphones, 5G is designed to serve as an industrial-grade operating system. Industry validation indicates that 5G's economic impact is highly concentrated across three primary high-value domains:

-

Healthcare Applications: Projected to contribute USD 530 Billion to global GDP via remote surgery frameworks, real-time patient monitoring systems, and connected ambulance networks.

-

Smart Utilities Management: Expected to drive an additional USD 330 Billion in economic efficiency by linking wide-area smart grids and real-time consumption trackers.

-

Consumer and Media Implementations: Contributing USD 250 Billion through immersive cloud gaming, enhanced virtual/augmented reality (AR/VR), and high-bandwidth live streaming.

Combined with localized logistics, manufacturing automation, and municipal IoT deployments, the cumulative economic boost of widespread 5G integration is estimated to reach USD 1.3 Trillion, making current infrastructure deployments a critical focus for both enterprise leaders and public sector policymakers.

Strategic Market Dynamics: Analyzing the Primary Growth Catalysts

The remarkable 49.8% CAGR of the 5G infrastructure market is sustained by several structural market drivers:

-

Accelerated Industrial Digitization: Modern factories, automated warehouses, and port terminals require ultra-reliable low-latency communication (URLLC) to manage thousands of active autonomous guided vehicles (AGVs) and synchronized robotic arms simultaneously.

-

The Rise of High-Bandwidth Applications: High-definition video conferencing, real-time collaborative cloud environments, and high-tier AR/VR systems are outgrowing existing 4G and public Wi-Fi limits, forcing operators to deploy high-density small cell networks.

-

The Virtualization Paradigm Shift: Telecom operators are shifting rapidly from expensive, proprietary hardware appliances toward cloud-native software environments. This reduces long-term operational expenditures (OpEx) and enables rapid service scaling.

-

The Post-Pandemic Distributed Workforce: The structural shift toward hybrid and remote work models has permanently altered regional bandwidth demand, requiring service providers to expand high-frequency networks deep into residential and commercial suburbs.

Structural Headwinds: Addressing Deployment Obstacles and Capital Overhead

While the market trajectory remains highly aggressive, the report balances its optimism with an unvarnished review of current industry constraints:

-

Substantial Upfront Capital Expenditures (CapEx): Building comprehensive dense network configurations—especially above 6 GHz millimeter-wave setups—requires an enormous volume of physical installations, fiber-optic backhaul links, and hardware acquisitions.

-

Complex Regulatory and Spectrum Allocations: Telecommunications operators must navigate intricate government auction frameworks, international spectrum harmonization rules, and local zoning laws to secure municipal permits for small cell placement.

-

Escalating Cybersecurity and Privacy Realities: By transitioning from fixed physical hubs to a software-driven, decentralized edge architecture, the potential digital attack surface multiplies. This demands advanced zero-trust security frameworks across both core and radio access networks (RAN).

Segment Analysis: Identifying Core Pillars of Network Evolution

The study segments the global 5G infrastructure market across multiple layers to offer clear visibility into emerging technology trends and capital deployment channels.

By Network Architecture: Non-Standalone (NSA) Dominates Early Deployment

In 2023, the 5G New Radio (NR) Non-Standalone (NSA) segment commanded a dominant 92.9% share of the global market. The overwhelming majority of initial 5G network roll-outs have been built directly on top of pre-existing 4G LTE physical cores. This architectural strategy has allowed major global telecom operators like AT&T, Verizon, and China Mobile to rapidly deploy 5G coverage footprints without immediately needing a costly, complete overhaul of their core network assets. This phase has successfully met initial consumer demand for cloud gaming and ultra-high-definition (UHD) streaming.

However, as enterprise demands shift toward advanced features like network slicing and pure URLLC, the industry is preparing for a gradual transition toward 5G Standalone (SA) architectures that operate completely independent of legacy systems.

By Core Network Technology: Network Function Virtualization (NFV) Leads Innovation

Within core software frameworks, Network Function Virtualization (NFV) held a majority market share in 2023. NFV transforms traditional hardware-bound networking elements (like firewalls, routers, and load balancers) into flexible software functions running on standardized, off-the-shelf commercial servers.

This model allows network operators to spin up virtual instances instantly wherever capacity demands fluctuate, eliminating the need to purchase and manually install expensive, single-use physical appliances. This scalability makes NFV an indispensable architecture for managing complex 5G network slicing and multi-access edge computing (MEC).

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/15292/

Deep Dive into Operational Frequency Bands: Sub-6 GHz vs. Millimeter Wave

Maximizing 5G performance relies heavily on spectrum strategy, requiring operators to balance coverage distance against data throughput speed.

-

Sub-6 GHz (Low and Mid-Bands): This frequency spectrum represents the foundational baseline for broad geographic 5G coverage. Offering an optimal balance between reliable signal propagation distances, deep building penetration, and competitive data speeds, Sub-6 GHz forms the practical core of suburban and urban mobile data networks worldwide.

-

Above 6 GHz (Millimeter Wave / mmWave): Representing high-frequency bands like 26 GHz and 28 GHz, this segment is growing rapidly. While millimeter-wave frequencies have short propagation distances and struggle with physical obstacles, they offer massive data capacities and near-zero latency. Governments and regulators are prioritizing global spectrum harmonization above 24 GHz, which will reduce device complexity, unlock economies of scale, and accelerate the roll-out of ultra-dense connectivity zones across crowded stadiums, transit hubs, and automated industrial plants.

Regional Perspectives: Asia-Pacific Outpaces Global Capital Expenditure

Asia-Pacific: The World's Engine for High-Density 5G Deployment

In 2023, Asia-Pacific secured the largest market share in the global 5G infrastructure ecosystem. This leading position is driven by massive, state-backed capital deployments and aggressive network expansions executed by leading communication service providers, including China Mobile Limited, KT Corporation, and NTT Docomo Inc. Furthermore, proactive regulatory bodies across Japan, South Korea, and China have streamlined access to vital sub-6GHz and millimeter-wave frequencies, fueling a rapid surge in domestic 5G subscribers and broad ecosystem growth.

North America: Leading High-Value R&D and Enterprise Deployments

North America—predominantly driven by the United States market—is projected to grow at a remarkable CAGR through 2030. Regional expansion is fueled by deep investments in next-generation network R&D, a strong concentration of global tech pioneers, and rapid commercial adoption of private 5G networks across industrial environments. The region's emphasis on high-margin software innovation, open-RAN architectures, and enterprise cloud integrations keeps it at the forefront of global network evolution.

Europe: Structured Modernization and Strict Industrial Integration

Europe is advancing through a structured modernization roadmap, focused on integrating 5G networks into its advanced automotive, maritime logistics, and high-precision manufacturing industries. Major operators across Germany, the UK, and France are actively collaborating with industrial leaders to deploy dedicated private 5G networks, ensuring highly secure, low-latency operational environments.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/global-5g-infrastructure-market/15292/

Competitive Intelligence: Key Market Leaders Steering Next-Gen Networks

The global 5G infrastructure landscape is highly competitive, led by prominent telecom hardware manufacturing giants and enterprise cloud software innovators. To maintain market share, these companies heavily prioritize research and development, forge deep partnerships with cloud providers, and actively support the shift toward open, interoperable network standards.

5G Infrastructure Market, Key Players

1. Analog Device

2. Cavium

3. Cisco Systems

4. Ericsson

5. Fujitsu

6. Huawei Technologies Co. Ltd.

7. Intel Corporation

8. LG Electronics Inc.

9. MACOM Technology Solutions

10. MediaTek Inc.

11. NEC Corporation

12. Qorvo

13. Qualcomm

14. Samsung

15. VMware

16. AT&T

17. Nokia

18. Verizon Communication

19. T-Mobile

20. ZTE Telecom

21. Networks Inc.

22. SK Telecom Co. Ltd.

23. Hewlett Packard Enterprise

24. Korea Telecom

25. China Mobile

Clear Market Vision: Critical Strategic Decisions for Telecommunications Executives

To maximize return on investment and build resilient network environments over the next decade, decision-makers should focus on four core priorities:

-

Accelerate the Core Migration to Standalone (SA) 5G: While Non-Standalone networks were effective for initial consumer roll-outs, capturing high-margin enterprise value requires migrating to cloud-native Standalone architectures. This shift unlocks essential capabilities like network slicing, multi-access edge computing, and ultra-reliable low-latency communications.

-

Embrace Virtualization and Open-RAN Models: Transitioning away from proprietary hardware ecosystems toward software-defined virtualization helps reduce vendor lock-in, optimizes operational spending, and allows operators to scale network capacity dynamically via automated software controls.

-

Monetize Enterprise Private 5G Networks: High-value growth is moving toward dedicated private networks tailored for automated manufacturing, remote mining, and smart logistics hubs. Providers should develop specialized packages combining local small cells, edge processing, and custom service-level agreements (SLAs).

-

Implement Advanced Zero-Trust Security: As software-driven edge connections expand, security models must adapt. Enterprise networks require deep visibility, continuous device authentication, and automated threat mitigation integrated into every layer of the infrastructure.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656