COVID-19 Diagnostics Market Analysis, Trends and Industry Outlook

Global COVID-19 Diagnostics Market Positioned to Reach USD 109.03 Billion by 2032, Driven by Multiplex Respiratory Screening and Institutional Surveillance, Reports Maximize Market Research

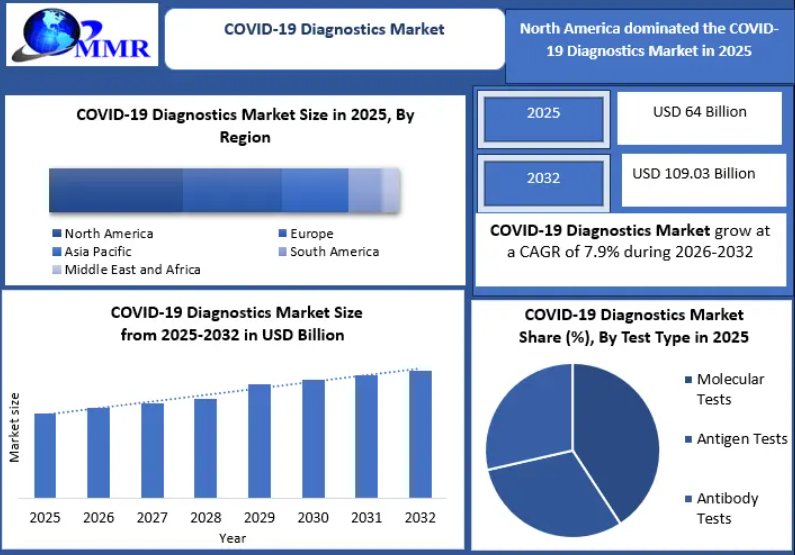

The global medical infrastructure is experiencing a profound paradigm shift as infectious disease management transitions from crisis-driven emergency responses to sustainable, multi-pathogen surveillance strategies. According to a comprehensive market intelligence report published by Maximize Market Research, the Global COVID-19 Diagnostics Market, which was valued at USD 64 Billion in 2025, is structurally positioned to expand to USD 109.03 Billion by 2032. This robust market evolution represents a calculated Compound Annual Growth Rate (CAGR) of 7.9% during the forecast period from 2026 to 2032.

As the healthcare landscape navigates the post-pandemic era, the reliance on high-precision testing has not diminished; rather, it has become deeply integrated into institutional protocols. Hospitals, diagnostic laboratories, corporate environments, international transit hubs, and municipal public health agencies are actively moving away from isolated single-pathogen testing. Instead, the focus has redirected toward targeted respiratory screening, genomic variant monitoring, and automated multiplex molecular systems. This long-term strategic evolution underscores the vital commercial and clinical relevance of the global diagnostics ecosystem.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/303441/

Strategic Market Vision: Shifting from Emergency Response to Endemic Surveillance

The transition of COVID-19 from a pandemic emergency to an endemic public health concern has systematically redefined the operational mandates of diagnostic manufacturers and clinical providers worldwide. During the peak years of the pandemic, the market was heavily shaped by volume-driven, unregulated distribution of single-pathogen tests. Today, the market operates on an enterprise-grade framework focused on long-term preparedness, data integration, and multi-disease differentiation.

Rather than rendering testing infrastructure obsolete, the standardization of respiratory care has firmly cemented COVID-19 diagnostics into regular medical practice. Clinical environments are prioritizing syndromic testing—where a single patient sample is processed to identify multiple potential pathogens simultaneously. This clinical progression guarantees that molecular diagnostic platforms will retain high capacity utilization and financial viability over the next decade.

Technological Innovation: The Rise of Multiplex Panels and Laboratory Automation

A primary engine powering the 7.9% CAGR of the global market is the accelerated deployment of next-generation multiplex Molecular Diagnostics (PCR/NAAT). Advanced molecular architectures now allow clinical systems to run automated, high-throughput assays capable of identifying up to six distinct respiratory targets simultaneously, including SARS-CoV-2, Influenza A/B, and Respiratory Syncytial Virus (RSV).

Key technical advancements that continue to reshape market dynamics include:

-

High-Throughput Automation: Modern integrated PCR platforms can systematically process between 1,000 and 4,000 samples per day per laboratory. By automating complex pipetting and amplification cycles, institutions have successfully mitigated manual testing errors by nearly 80%.

-

Turnaround Optimization: Through advanced microfluidic designs and rapid amplification chemistry, the time-to-result for centralized laboratory testing has been reduced by 20% to 50%. This enables acute-care facilities to make fast, evidence-based triage decisions.

-

AI-Assisted Diagnostics: The incorporation of artificial intelligence and machine learning algorithms into diagnostic software allows for automated curve analysis, variant identification, and immediate digital reporting to epidemiological surveillance networks.

Recent regulatory milestones emphasize this transition toward integrated solutions. For example, prominent industry leaders have secured formal FDA clearances and CE-IVDR approvals for comprehensive respiratory select panels, reinforcing the financial and operational wisdom of single-test, multi-pathogen procurement.

Comprehensive Market Segmentation Analysis

The global COVID-19 diagnostics landscape is highly diversified across testing technologies, clinical environments, and point-of-care distribution models.

By Test Type: Molecular Diagnostics Remains the Gold Standard

-

Molecular Diagnostics (PCR/NAAT): This segment continues to capture the largest market share. Renowned for its analytical sensitivity (ranging from 95% to 99%) and specific variant-tracking capabilities, Polymerase Chain Reaction (PCR) remains the mandatory confirmatory standard for global health systems. More than 85% of hospitals worldwide maintain rigid compliance protocols requiring molecular validation for symptomatic patients.

-

Rapid Antigen Tests: Operating as the fastest-growing technology segment, rapid antigen testing dominates decentralized environments. Its market expansion is sustained by extreme cost efficiency, immediate turnaround times (10 to 30 minutes), and massive consumer adoption through retail pharmacy channels for home-care screening.

-

Antibody (Serology) Tests: While less relevant for acute diagnosis, serology platforms maintain steady demand within academic research, longitudinal immunity studies, and large-scale population seroprevalence tracking conducted by non-governmental health organizations.

By End User: Centralized Power vs. Decentralized Speed

-

Hospitals & Diagnostic Laboratories: This segment holds the commanding share of global revenue. The necessity for high-volume processing, strict regulatory compliance, and complex differential diagnosis drives continuous institutional capital investment in molecular instruments, automated liquid handlers, and premium reagents.

-

Home Care & Point-of-Care (PoC) Settings: Emerging as a major growth vector, decentralized testing sites—including local clinics, workplace health centers, and home environments—are expanding rapidly. The democratization of diagnostic tools has altered patient behavior, making rapid self-testing an established social and professional norm.

Comprehensive Analytical Comparison of Core Diagnostic Modalities

To provide clear strategic direction for healthcare procurement officers, corporate buyers, and institutional laboratory directors, the operational differences between primary testing methodologies are outlined below:

| Feature/Parameter | Molecular Tests (PCR / NAAT) | Antigen Tests | Antibody (Serology) Tests |

| Primary Target | Viral genetic material (RNA) | Viral surface proteins (Antigens) | Host immune proteins (IgG/IgM) |

| Clinical Purpose | Definitive active infection confirmation | Rapid screening of infectious individuals | Assessment of historical exposure/immunity |

| Sample Matrix | Nasopharyngeal/Oropharyngeal swab, Saliva | Nasal or Nasopharyngeal swab | Whole blood, Serum, or Plasma |

| Turnaround Time | 20 mins (PoC) to 72 hours (Central Lab) | 10 to 30 minutes | 1 to 3 days (Batch processed) |

| Analytical Accuracy | Extremely High (Clinical Gold Standard) | Moderate (Dependent on viral load) | High (Variable by post-infection timeline) |

| Primary Advantage | Detects low viral loads; tracks variants | Low unit cost; immediate actionable data | Essential for epidemiological modeling |

| Primary Limitation | High infrastructure cost & staff expertise | Lower sensitivity; false-negative risks | Cannot be used to diagnose active disease |

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/303441/

Global Market Economics: Cost Configurations and Investment Realities

Navigating the financial landscape of the endemic diagnostics market requires an understanding of structural pricing models. The commercialization of testing solutions operates within distinct cost bands, which influence healthcare access and manufacturing margins across different geographic regions:

-

RT-PCR Test Kits (Per Test): USD 15 – USD 50 (Varies based on multiplex capabilities and regulatory validation).

-

Rapid Antigen Test Kits (Per Test): USD 3 – USD 15 (Highly competitive pricing driven by high-volume retail contracts).

-

Molecular Diagnostic Instruments: USD 15,000 – USD 150,000+ (Representing significant capital expenditure for modern laboratory facilities).

-

Sample Collection & Consumables: USD 2 – USD 10 (Swabs, transport media, and extraction plates).

-

Laboratory Automation & Integration Platforms: USD 20,000 – USD 200,000+ (Required for high-throughput, error-free institutional tracking).

Regional Dominance and Geographic Growth Drivers

North America: The Infrastructure Leader

North America safely commanded the largest market share in 2025 and is projected to maintain its financial leadership through 2032. The region’s dominant position is reinforced by a highly sophisticated molecular testing infrastructure, favorable and clear reimbursement frameworks (including Medicare and private insurer coverage), and multi-billion-dollar government allocations dedicated to national biosecurity and pandemic preparedness. Furthermore, the strong presence of global life science conglomerates—such as Thermo Fisher Scientific, Abbott Laboratories, Danaher Corporation, and BD—ensures immediate domestic supply chain stability and rapid adoption of newly cleared testing technologies.

Asia-Pacific: The Fastest Growing Marketplace

The Asia-Pacific region is analyzed to experience the highest compound growth rate through the forecast period. This commercial surge is fueled by massive public health expansions across emerging economies, notably India, China, and key ASEAN nations. Government-led mandates for localized medical device manufacturing are lowering production costs, while rising disposable income and expanding rural healthcare networks are driving the adoption of decentralized, point-of-care diagnostics. In addition, localized surveillance initiatives aimed at curbing seasonal respiratory outbreaks are securing sustained, long-term procurement pipelines for multi-pathogen testing kits.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/covid-19-diagnostics-market/303441/

Critical Market Restraints and Strategic Solutions

Despite a highly positive long-term growth forecast, the market faces structural challenges that require strategic agility from global suppliers:

-

Volume Normalization and Margin Pressures: The predictable decline in pure, un-targeted mass community screening has reduced standard revenue streams for commodity-grade antigen tests. The Solution: Savvy manufacturers are converting simple production lines into high-value multiplex kit assembly operations.

-

Infrastructure Barriers in Low-to-Middle-Income Countries (LMICs): High capital costs for molecular platforms limit advanced testing capabilities in developing economies. The Solution: The industry is responding with ruggedized, cartridge-based, point-of-care molecular machines that require minimal technical training and no complex laboratory infrastructure.

-

Workforce Deficits: A global shortage of certified medical laboratory scientists continues to create operational bottlenecks. The Solution: System designs are shifting heavily toward "plug-and-play" automation, allowing non-specialized staff to safely run complex testing sequences.

Clear Market Vision: Future Outlook and Strategic Recommendations

For venture capitalists, healthcare executives, and pharmaceutical decision-makers, the global COVID-19 diagnostics market represents a stable, highly sophisticated segment within the broader in-vitro diagnostics (IVD) industry. Success over the 2026–2032 forecast horizon requires a strong commitment to three core strategies:

-

Invest in Multi-Pathogen Panels: Future profitability belongs to companies that integrate SARS-CoV-2 detection seamlessly into general respiratory, gastrointestinal, or sexually transmitted disease panels.

-

Focus on Point-of-Care Molecular Formats: The market heavily rewards platforms that combine the near-perfect accuracy of traditional PCR with the 20-minute speed and simplicity of lateral flow antigen tests.

-

Strengthen Digital Integration: Software that securely binds diagnostic results to corporate health platforms, international travel passes, or government epidemiological portals will win long-term contract preferences.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656