Cardiac Rhythm Management Devices Market Outlook 2025: Innovation, Market Dynamics, and Future Opportunities

FOR IMMEDIATE RELEASE

Global Cardiac Rhythm Management Devices Market to Reach USD 32.05 Billion by 2032, Driven by a 6.14% CAGR, Leadless Miniaturization, and AI Remote Patient Monitoring

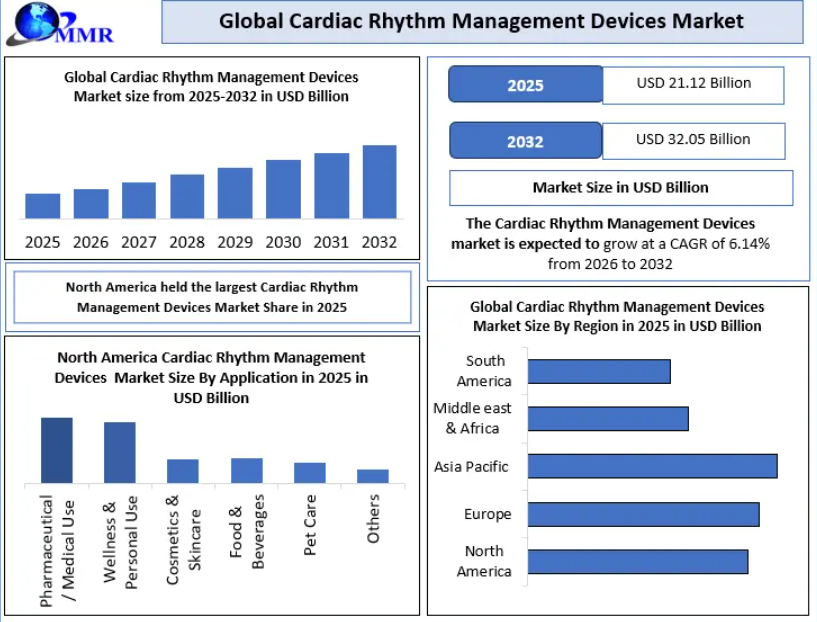

an authoritative global business intelligence and healthcare consulting firm, has released its highly anticipated definitive intelligence study on the Global Cardiac Rhythm Management (CRM) Devices Market. The exhaustive, data-verified report indicates that the market, valued at USD 21.12 Billion in 2025, is positioned for steady, structural expansion, projected to achieve a market evaluation of USD 32.05 Billion by 2032. This robust growth trajectory represents a stable Compound Annual Growth Rate (CAGR) of 6.14% over the forecast period from 2026 to 2032.

The report highlights a deep clinical and technological shift in modern electrophysiology. The global CRM devices market is no longer solely reliant on traditional transvenous hardware configurations. Instead, it is increasingly dominated by next-generation leadless pacemakers, ultra-miniaturized implantable cardioverter-defibrillators (ICDs), and cloud-integrated, artificial intelligence (AI)-powered remote patient monitoring platforms. These innovations are transforming management frameworks for heart failure and complex cardiac arrhythmias from reactive emergency clinical treatments into highly automated, preventative digital health ecosystems.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/302269/

The Path to Proactive Electrocardiology: Key Structural Drivers

The global cardiovascular health landscape is facing an unprecedented demand shock. According to Maximize Market Research statistical modeling, over 38 million individuals globally are currently living with diagnosed atrial fibrillation (AFib), while ventricular arrhythmias remain the underlying clinical cause for roughly 75% to 80% of sudden cardiac death (SCD) cases worldwide. This expanding patient demographic, heavily exacerbated by an aging global population and a rising incidence of metabolic co-morbidities, serves as the primary clinical demand engine driving long-term market procurement.

The current phase of market expansion is fueled by three critical technological breakthroughs:

-

Clinical Adoption of Leadless Systems: Minimally invasive, self-contained capsules implanted directly inside the cardiac chamber have reduced post-operative complication rates by over 60% compared to traditional wired systems.

-

AI-Enabled Remote Diagnostic Platforms: Continuous, cloud-linked data streams from embedded devices allow clinical algorithms to predict potential tachyarrhythmia episodes up to 48 hours in advance, reducing emergency hospital readmissions by 51%.

-

The Expansion of MRI-Compatible Architectures: The absolute standardization of full-body 1.5T and 3T MRI-compatible systems has eliminated a historical barrier to implantation, enabling chronic disease patients to undergo essential diagnostic imaging safely throughout their lifespans.

Granular Market Segmentation and Strategic Data Insights

To equip corporate planners, healthcare hospital networks, venture capital firms, and medical device manufacturers with a clear market vision, the study segments the global CRM landscape across three core pillars: Product Type, Technology Infrastructure, and End-User Distribution.

1. By Product Type: Pacemakers Maintain Volume Dominance While ICDs Command High Value

-

Cardiac Pacemakers: This segment retained the largest operational footprint, accounting for approximately 42.2% of total global market revenue in 2025. Widespread clinical adoption is supported by an astonishing global volume of roughly 1.25 million pacemaker implantations performed annually. Within this segment, single-chamber and dual-chamber conventional setups are facing heavy substitution pressures from high-margin leadless options.

-

Implantable Cardioverter Defibrillators (ICDs): Representing the largest absolute capital asset sub-segment, ICDs continue to experience steady pull due to their role in preventing sudden cardiac arrests. The market is shifting from transvenous systems toward Subcutaneous Implantable Cardioverter Defibrillators (S-ICDs), which avoid the vascular system entirely and eliminate long-term lead-fracture risks.

-

Cardiac Resynchronization Therapy (CRT) Devices: Comprising both CRT-Pacemakers (CRT-P) and CRT-Defibrillators (CRT-D), this specialized segment is recording the fastest adoption curves among heart failure patients exhibiting left ventricular dyssynchrony.

-

External Defibrillators: This includes Automated External Defibrillators (AEDs) and Wearable Cardioverter Defibrillators (WCDs). WCDs are enjoying a strong demand wave as a bridge therapy for patients recovering from acute myocardial infarctions who do not yet meet standard criteria for permanent ICD placement.

2. By Technology Infrastructure: The Leadless and Remote Connected Wave

-

Leadless & Miniaturized Systems: This technical segment is seeing rapid growth. Modern dual-chamber leadless systems, such as Abbott's AVEIR DR and Medtronic's Micra AV2, are achieving clinical implantation success rates approaching 98%, expanding the candidate pool to include high-risk geriatric and pediatric cohorts.

-

Remote Monitoring & Wireless Connectivity: Device ecosystems equipped with Bluetooth Low Energy (BLE) and automated cellular home communicators have transitioned from an premium feature into an industry standard.

-

Wearables & Digital Health Platforms: Patch-based Holter surrogates and consumer-grade smart wearables are expanding the diagnostic funnel, identifying millions of previously asymptomatic paroxysmal AFib patients and funneling them directly into electrophysiology clinics for permanent CRM device installation.

3. By End-User Distribution: Hospitals Lead but ASCs Gain Ground

-

Hospitals and Specialized Cardiac Centers: These facilities continue to command over 65% of absolute implantation volumes, owing to the presence of dedicated electrophysiology (EP) labs, complex surgical infrastructure, and established insurance reimbursement channels.

-

Ambulatory Surgical Centers (ASCs): Driven by structural changes in Medicare and private payer reimbursement schedules, uncomplicated routine CRM procedures—specifically pacemaker replacements and single-chamber leadless installations—are migrating rapidly to lower-cost outpatient ambulatory environments.

In-Depth Market Dynamics: Macroeconomic Drivers & Constraints

The Economics of Longevity and Payer Cost Compression

The primary economic force shaping the medical technology sector is the financial burden of managing chronic heart failure. Hospital readmissions for heart failure place a heavy strain on public and private insurance frameworks. A standard heart failure re-hospitalization event in Western economies incurs an average institutional cost ranging from USD 17,500 to USD 24,000.

By utilizing advanced CRM architectures integrated with continuous pulmonary artery pressure indices and real-time thoracic impedance tracking, clinical teams can execute proactive pharmacological adjustments remotely. This data-driven, preventive treatment model helps mitigate acute decompensation episodes, compressing heart failure-related hospital expenditures by over 50%. This proven clinical utility has led major insurance groups to implement favorable coverage schedules, accelerating device adoption.

The Miniaturization Paradigm and the Elimination of Lead Failures

Historically, the primary point of failure in long-term cardiac pacing has been the transvenous lead. Traditional leads are vulnerable to insulation degradation, venous thrombosis, structural fractures, and bacterial endocarditis, frequently requiring dangerous extraction procedures. The transition toward leadless designs addresses these challenges directly.

By housing the pulse generator, lithium-carbon monofluoride battery cell, and biocompatible fixation tines within a single, ultra-compact capsule smaller than a standard AAA battery, leadless devices eliminate pocket infections and lead dislodgement risks. Furthermore, advancements in battery chemistry have extended the operational lifespan of these miniaturized systems to between 12 and 17 years, effectively matching or exceeding the longevity of traditional larger systems.

Regulatory Rigor and Supply Chain Imperatives

While the clinical demand for CRM systems remains robust, the market operates under stringent regulatory requirements. The transition from the legacy Medical Device Directive (MDD) to the rigorous European Medical Device Regulation (EU MDR) has created temporary friction. The heightened demand for extensive, long-term post-market clinical follow-up data has extended product clearance timelines for mid-tier innovators by an average of 18 to 26 months.

Additionally, medical-grade semiconductor supply chains remain highly consolidated. The production of specialized, ultra-low-power microcontrollers and telemetry chips requires dedicated cleanroom allocation from foundational silicon foundries, exposing CRM device suppliers to raw material price volatility and macroeconomic component backlogs.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/302269/

Regional Market Analysis: North America Leads, Asia-Pacific Surges

North America (The Technological and Volume Anchor)

North America continues to hold the largest market share, commanding approximately 42.58% of global CRM revenue in 2025. The region's position is anchored by an exceptional rate of clinical adoption for leadless configurations, with North America representing roughly 50% of the world's total leadless pacemaker implantation volume. Growth is further accelerated by high healthcare capital expenditure, widespread integration of cardiology informatics across major hospital groups, and the presence of industry-defining market leaders.

Asia-Pacific (The Growth Engine)

The Asia-Pacific marketplace is projected to expand at the fastest pace through 2032. This rapid growth is driven by the escalating cardiovascular disease burden across highly populated economies including China, India, Japan, and South Korea. Government-backed medical access expansions, such as India’s Ayushman Bharat infrastructure initiative, are making advanced cardiovascular interventions accessible to millions of previously underserved patients. This expansion is driving high procedural volumes for basic and intermediate pacing architectures.

Europe (The Hub for Advanced Regulatory Approvals)

Europe maintains a steady, resilient market position, often serving as the primary incubator for early-stage clinical evaluations of next-generation CRM technology. The region exhibits high clinical penetration for cardiac resynchronization therapy platforms, supported by centralized universal healthcare systems that prioritize therapies with long-term, proven reductions in secondary hospitalization rates.

+---------------------------------------------------------------------------------+

| GLOBAL CRM MARKET SHARE BY REGION |

+---------------------------------------------------------------------------------+

| [North America: ~42.58%] --> Dominates via Leadless Tech & Advanced Informatics |

| [Europe: Stable & Resilient] --> Leads in Early-Stage CRT Penetration |

| [Asia-Pacific: Fastest Growth] --> Driven by Massive Patient Volume Expansion |

+---------------------------------------------------------------------------------+

Competitive Intensity Mapping and Strategic Innovation Matrices

The global cardiac rhythm management landscape is characterized by a highly concentrated, capital-intensive competitive core. A small group of medical technology giants commands the majority of global market share through extensive patent portfolios, established hospital procurement contracts, and massive annual research and development investments.

Strategic Key Industry Competitors Profiled:

-

Medtronic plc (Ireland)

-

Abbott Laboratories (United States)

-

Boston Scientific Corporation (United States)

-

BIOTRONIK SE & Co. KG (Germany)

-

Koninklijke Philips N.V. (Netherlands)

-

MicroPort Scientific Corporation / MicroPort CRM (China / France)

-

Zoll Medical Corporation (United States)

-

LivaNova PLC (United Kingdom)

-

Nihon Kohden Corporation (Japan)

-

Schiller AG (Switzerland)

Market leaders are actively executing strategic mergers, acquisitions, and collaborative partnerships to integrate clinical software capabilities directly into their hardware portfolios. The competitive focus has shifted from pure mechanical durability to algorithmic intelligence. Companies are actively competing to develop superior machine learning models capable of filtering out signal artifacts from wearable devices, ensuring that only highly accurate, actionable telemetry data reaches clinical electrophysiologists.

Value Chain Assessment: Shift Toward Software Integration

An analytical review of the CRM industry value chain shows that value generation is moving away from basic structural hardware toward software intelligence layers and data analytics.

+---------------------------------------------------------------------------------+

| CRM DEVICE MARKET VALUE CHAIN |

+---------------------------------------------------------------------------------+

| Specialized Alloys/Sensors --> Advanced Micro-Assembly --> AI Telemetry Layer |

| (Low Margin / High Volume) (Traditional Hardware) (High Margin Engine) |

+---------------------------------------------------------------------------------+

| *Long-term value is increasingly driven by predictive diagnostic algorithms.* |

+---------------------------------------------------------------------------------+

While specialized raw material refinement (such as biocompatible titanium castings and platinum-iridium electrode tips) operates on standard manufacturing margins, the proprietary software layer—encompassing encrypted telemetry protocols and AI-driven arrhythmia detection algorithms—represents a major high-margin engine for the industry. Established companies are leveraging this trend by packaging their physical implants with cloud-based patient management software platforms, building strong ecosystem integration that encourages long-term hospital group loyalty.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/cardiac-rhythm-management-devices-market/302269/

Strategic Action Framework for Healthcare Decision-Makers

For hospital executive boards, medical directors, and healthcare investors, the evolution of the CRM market requires a shift in procurement and deployment strategies:

-

Evaluate Total Cost of Ownership (TCO): When assessing high-cost leadless or subcutaneous devices, procurement committees should look beyond the initial premium purchase price. Financial models should account for long-term savings from reduced lead extractions, lower post-operative infection management costs, and fewer follow-up clinic visits.

-

Invest in Scalable Cardiology Informatics: Hospital groups must ensure their IT infrastructure can securely ingest, organize, and analyze the large volume of remote telemetry data generated by modern BLE-enabled implants without overwhelming clinical teams.

-

Establish Clear Outpatient Migration Strategies: Given the ongoing shift of routine pacing procedures toward ambulatory settings, healthcare systems should optimize their ASC workflows to maintain high efficiency and capture profitable outpatient procedural volumes.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656