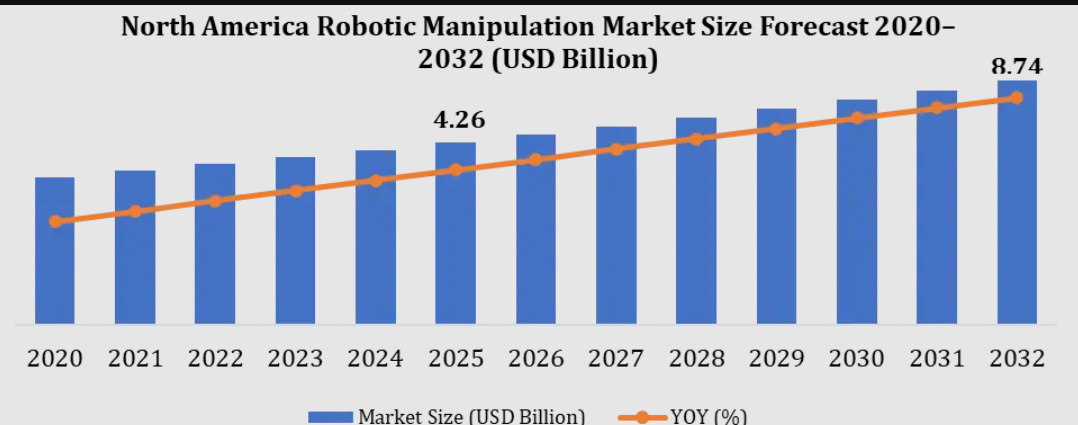

North America Robotic Manipulation Market Share, Revenue and Future Forecast

North America Robotic Manipulation Market Set for Substantial Growth, Fueled by Reshoring Mandates, Advanced AI-Driven Logistics, and Autonomous Manufacturing Networks

A leading global business intelligence and market consulting firm, has released its highly anticipated and comprehensive industry analysis on the North America Robotic Manipulation Market. The exhaustive study delivers an analytical, multi-dimensional evaluation of the advanced automation landscape, mapping out structural growth catalysts, technological transitions, supply chain dynamics, and competitive operational strategies.

The new publication reveals that the North American robotic manipulation sector is undergoing a profound structural evolution. Driven by intense domestic manufacturing reshoring mandates, persistent regional skilled labor shortages, and rapid integration of generative artificial intelligence (AI) and multimodal vision systems, market demand is climbing toward unprecedented milestones. The analysis emphasizes that the strategic convergence of cloud-edge compute infrastructure with high-dexterity hardware has positioned the United States, Canada, and Mexico as primary focal points for high-margin, software-defined industrial automation installations.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/306269/

Executive Summary: Strategic Re-shoring and the Next Wave of Industrial Autonomy

The macro-industrial ecosystem in North America has evolved past the era of isolated, deterministic automation. Today, advanced robotic manipulation—comprising multi-axis articulated arms, cartesian systems, SCARA configurations, delta pickers, and force-sensitive collaborative robots (cobots)—serves as the foundational blueprint for modern supply chain resilience.

Geopolitical realignments, shifting trade policies, and recent historical supply chain vulnerabilities have forced North American enterprises to bring manufacturing back home. However, to remain competitive against low-cost overseas labor pools, domestic manufacturers must optimize their floor efficiency. Robotic manipulation systems fill this gap.

The market intelligence report breaks down the industry across several critical verticals: by component (hardware, cloud-connected software, and system integration services), by payload capacities (lightweight under 10 kg, mid-range 10–50 kg, heavy-duty 50–200 kg, and ultra-heavy payloads exceeding 200 kg), by application (high-speed picking and placing, precise assembly, heavy material handling, welding/cutting, and cleanroom semiconductor processing), and by key end-user segments (automotive/EV manufacturing, aerospace and defense, food & beverage processing, medical devices/pharmaceuticals, and hyper-scale e-commerce logistics).

Core Market Dynamics: Macroeconomic Catalysts Driving Regional Expansion

A deep dive into the North American robotic manipulation market highlights several fundamental economic and technological drivers that are accelerating multi-industry capital expenditure (CapEx).

1. The Automation Mandate: Mitigating a Structural Labor Deficit

North American manufacturers are facing a severe, long-term shortage of skilled labor. A significant portion of the specialized welding, assembly, and machining workforce is reaching retirement age, while younger generations are pursuing fewer traditional manufacturing careers. This ongoing labor deficit is driving companies to automate repetitive, physically demanding, and hazardous floor tasks. Integrating advanced robotic manipulation helps fill this operational gap, allowing companies to redirect their remaining human talent to higher-value positions like system optimization, predictive maintenance scheduling, and fleet management.

2. Generative AI, VLA Models, and Unstructured Object Perception

Historically, industrial arms operated within rigid parameters—they could only interact with items placed in exact, predetermined spatial orientations. The modern North American market is breaking away from these programming limitations through the deployment of Vision-Language-Action (VLA) models and decentralized edge processing. Equipped with high-resolution 3D sensors and advanced neural networks, modern robotic manipulators can accurately evaluate and sort mixed, unstructured parts from random bins, adapt in real time to shifting product shapes, and dynamically alter their tool paths to optimize cycle times.

3. Hyper-Scale E-Commerce Fulfillment and High-Throughput Intralogistics

The rapid expansion of high-velocity, same-day delivery networks across North America has placed intense pressure on the logistics sector. Warehouses must handle thousands of variable stock-keeping units (SKUs) with near-zero error margins. This demand is accelerating the deployment of robotic manipulators mounted on Autonomous Mobile Robots (AMRs) or fixed at critical induction points. These systems manage high-speed sorting, parcel singulation, mixed-case palletization, and complex order picking, turning traditional distribution hubs into highly flexible, automated operations.

Segment Analysis: Identifying High-Growth Technical Sub-Sectors

A granular look at the market structure reveals specific sub-segments that are drawing major corporate investment and technological interest.

Software Integration as the Core Value Acceleration Engine

While robust mechanical components—such as low-backlash planetary gearboxes, high-torque servo drives, and custom end-of-arm tooling (EoAT)—account for a large portion of initial hardware budgets, the software and subscription service segment is projected to achieve the fastest growth rate. The primary source of value within the robotics space is shifting decisively toward intelligent orchestration software layers. Multi-vendor robotic fleets now require unified, cloud-connected platforms that leverage artificial intelligence for real-time kinematic path calculation, asset health tracking, and predictive maintenance to minimize unplanned factory downtime.

The Rise of Flexible, Safety-Monitored Collaborative Robots (Cobots)

Traditional high-payload industrial robots have long required heavy, isolated security fencing due to their high kinetic energy and lack of ambient sensory awareness. The collaborative robotics segment is dismantling these physical floor boundaries. Built with integrated joint torque sensors, capacitive proximity skins, and force-limiting control algorithms, modern cobots are designed to work safely alongside human operators. This segment is growing rapidly among small and medium-sized enterprises (SMEs) across North America, as cobots offer a compact physical footprint, lower initial installation barriers, and straightforward programming environments that do not require specialized robotics engineers.

Regional Developments: United States, Canada, and Mexico

The geographic footprint of the North American robotic manipulation market features a highly integrated, cross-border supply chain network, with each nation fulfilling a distinct industrial role.

United States: The Hub for Advanced AI, Aerospace, and High-Value Automation

The United States represents the largest market share and technology development core within the region. Driven by major capital investments in electric vehicle (EV) gigafactories, next-generation aerospace programs, and massive e-commerce fulfillment hubs, U.S. enterprises are prioritizing advanced, software-heavy robotic infrastructure. The country is a leading hub for venture capital funding in robotics software, cloud-based fleet orchestration platforms, and adaptive AI vision systems, moving the domestic market toward highly intelligent, autonomous operations.

Mexico: Automotive Nearshoring and High-Velocity Assembly Infrastructure

Mexico is experiencing a major manufacturing boom, driven by intense nearshoring trends as companies move production closer to North American consumer markets. Guided by the USMCA trade agreement, global automotive brands and electronics OEMs are upgrading their Mexican production facilities. This industrial expansion has created a surge in demand for heavy-duty multi-axis articulated robots for precision automotive body welding, structural part handling, and high-volume electronics assembly, establishing Mexico as a key region for industrial hardware installation.

Canada: Advanced Food Processing, AgTech, and Natural Resource Logistics

The Canadian market is defined by a strong focus on advanced food and beverage packaging, agricultural technology, and natural resource supply chain management. Confronting tight labor markets across rural manufacturing hubs, Canadian processing facilities are increasingly turning to delta pickers and vision-guided SCARA arms to handle delicate products, optimize food safety compliance, and automate continuous secondary packaging lines under strict environmental standards.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/306269/

Strategic Implementation Framework for Enterprise Leaders

Successfully deploying an advanced robotic manipulation network requires a strategic, phased approach that addresses both technical integration and organizational readiness.

Industry Bottlenecks: Addressing Integration Challenges and Skill Gaps

While the economic advantages of automation are clear, enterprise buyers must navigate specific operational challenges to ensure successful, long-term implementations.

Legacy Infrastructure and Communication Silos

A significant challenge on brownfield factory floors across North America is integrating new, high-speed robotic manipulators with older, legacy manufacturing equipment. Older machinery often uses proprietary communication protocols, creating data silos that complicate integration. Achieving smooth synchronization between a modern, AI-enabled robotic controller, a legacy PLC network, and an enterprise Manufacturing Execution System (MES) requires comprehensive industrial communication planning and a commitment to open communication frameworks like OPC Unified Architecture (OPC UA).

The Advanced Automation Skills Gap

As robotic manipulation hardware becomes more advanced and software-driven, the skill set required to maintain and optimize these systems has shifted. Many manufacturing facilities face a gap in internal technical expertise, lacking personnel who understand both physical automation hardware and advanced software layers like ROS-Industrial, machine vision calibration, and edge compute diagnostics. Companies must invest in structured workforce training programs and collaborate with system integrators to ensure their teams can effectively manage these automated systems day-to-day.

Competitive Intelligence: Key Vendors and Strategic Directions

The North American robotic manipulation market features a highly competitive landscape, driven by established global automation providers alongside specialized regional software and system integrators. Key market participants evaluated in the report include:-

1. ABB Ltd.

2. FANUC Corporation

3. KUKA AG

4. Rockwell Automation

5. Teradyne

6. Universal Robots

7. Yaskawa Electric Corporation

8. NVIDIA Corporation

9. Amazon Robotics

10. Zebra Technologies

11. Honeywell International

12. Omron Corporation

13. Siemens AG

14. Boston Dynamics

15. Teradyne Robotics

16. DENSO Robotics

17. GreyOrange

18. Fetch Robotics

19. Locus Robotics

20. Kawasaki Robotics

The primary competitive strategies in this region focus on expanding regional technical support networks and forming joint ventures with specialized AI software developers. Top-tier vendors are focusing on providing out-of-the-box, application-specific robotic kits—such as pre-engineered robotic welding cells or vision-guided palletizing packages—that simplify the purchasing process, speed up installation timelines, and reduce the integration risks for end-users.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/north-america-robotic-manipulation-market/306269/

Strategic Outlook: The Era of Connected, Adaptive Manufacturing

Looking forward, the North American robotic manipulation market is moving beyond standalone, single-task applications. The future of the region's manufacturing infrastructure lies in highly connected, software-defined production networks. As industrial 5G networks deploy across major manufacturing corridors, they will provide the low-latency wireless communication needed to run centralized AI models that coordinate teams of mobile and stationary manipulation systems in real time.

For executive decision-makers, operations directors, and investment planners, upgrading to advanced robotic manipulation is an essential requirement for maintaining long-term competitiveness. Investing in flexible, adaptive automation architectures today ensures that a company's production infrastructure can quickly adjust to changing product designs, unexpected labor fluctuations, and evolving global supply chain conditions tomorrow.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656